PUBLIC SECTOR BANKS (PSBs) BACKDROP

- The banking structure of India is headed by the RBI and comprises commercial and cooperative banks. Commercial banks include Scheduled Commercial Banks (SCBs) and non-scheduled commercial banks. SCBs, in turn, are divided into private, public, and foreign banks as well as Regional Rural Banks (RRBs), whereas co-operative banks comprise urban and rural lenders.

- Public Sector Banks (PSBs) are an important type of government-owned bank in India. A majority stake (> 50%) is held by the Ministry of Finance of the Government of India or State Ministries of Finance of different State Governments. In India, public sector banks play a dominant role in extending loans and collecting deposits, although over the years competition has substantially increased due to the emergence of the private sector and foreign banks.

- Public sector banks (PSBs) accounts for roughly 70% of total deposits, while private sector banks held the majority of the remaining.

- In India, 10 public sector banks (PSBs) were merged into four on 1 April 2020. Six weaker banks were merged with four larger, anchor banks. This merger has not only reduced the need for recapitalization from the government but also enabled smaller banks to benefit from the service delivery and technological prowess of larger banks. Union Bank of India absorbed Andhra Bank and Corporation Bank, while Oriental Bank of Commerce and United Bank merged with Punjab National Bank. Allahabad Bank merged with Indian Bank and Syndicate Bank merged with Canara Bank. Dena Bank and Vijaya Bank were merged with Bank of Baroda in 2019. With this, the total number of PSBs in India came down from 27 in 2017 to 12. These 12 banks now consist of six merged banks – SBI, Bank of Baroda, Punjab National Bank, Canara Bank, Union Bank of India and Indian Bank.

- The acquirer PSB banks, therefore, benefitted from a larger capital base and the regional presence of smaller banks with customers having access to a wider array of products and services to choose from in addition to traditional products like deposits and loans.

FINANCIAL PERFORMANCE

1. Market share of Major Public Sector Banks (%)

| Rank | Bank Name | 2016-17 | 2017-18 | 2018-19 | 2019-20 | 2020-21 |

| 1 | State Bank of India | 18.45 | 22.2 | 22.19 | 22.63 | 22.73 |

| 2 | Punjab National Bank | 5.31 | 5.15 | 4.94 | 4.78 | 6.6 |

| 3 | Bank of Baroda | 5.03 | 4.87 | 4.82 | 6.65 | 6.2 |

| 4 | Canara Bank | 4.27 | 4.34 | 4.47 | 4.3 | 6.12 |

| 5 | Union Bank of India | 3.38 | 3.34 | 3.1 | 3.11 | 5.62 |

2. Operating and Net Profit Margins

- All PSBs managed to record an expansion in their profit margins during the latest quarter of June 2021. Operating profits margins expanded on the back of lower interest expenses vis-à-vis interest income

- State Bank of India (SBI) recorded a rise in its operating margins from 22.2 per cent in the year-ago quarter to 24.5 per cent, although the rise was nominal when compared to its peers on account of higher interest costs.

- Punjab National Bank’s (PNB’s) interest income came down a tad, but the corresponding fall in interest expenses was much higher resulting in an expansion in both, operating and net profit margins. The operating profit margin recorded a strong expansion from 21.7 per cent during the June 2020 quarter to 27.1 per cent during the June 2021 quarter.

3. Net Interest Margin (NIM)

- SBI has the highest NIM of more than three per cent throughout the year. For the latest quarter of June 2021, SBI’s NIM stood at 3.15 per cent followed by Union Bank of India at 3.08 per cent.

- Bank of Baroda stood third with a NIM of 3.04 per cent.

- Both PNB and Canara Bank reported NIMs of less than three per cent.

4. Gross Non- Performing Assets (GNPA)

- SBI had the lowest GNPA in June 2021 quarter of about 5.3%

- PNB had a double-digit GNPA ratio through all the quarters. Its GNPA ratio stood at 14.3 per cent during the June 2021 quarter.

5. Deposit Growth

- Deposit growth accelerated from 7.9 per cent during the 2019-20 financial year to 11.4 per cent during the pandemic year of 2020-21. Within bank deposits, demand deposits increased at a faster pace than time deposits. The reason for the same was to be prepared for the contingencies related to health

KEY PSB INSIGHTS

GROWTH OPPORTUNITIES

- OPPORTUNITIES IN MOBILE BANKING- Mobile banking transaction volume and value increased y/y in FY2021 by 83% and 59%. Banks have ramped up their efforts to expand their footprints in this platform since the trend is likely to continue even after the pandemic.

- ADOPTING THE FINTECH TREND - In 2025, the fintech market in India is expected to grow to $ 84bn from its current value of $31bn. In terms of transaction value size, the fintech market is expected to grow to $ 138bn in 2023. These forecasts are backed up by the rising prominence of the fintech market plus its potential given the untapped population in India and the expected rise of both the middle- and high-income segments.

- KEY GOVT INITIATIVES- National Asset Reconstruction Company Limited (NARCL) which was recently announced by Nirmala Sitaraman will acquire stressed assets worth about Rs 2 lakh crore from various commercial banks in different phases. This is beneficial for every commercial bank as it will help them to clear off toxic assets in their books, which will help in enhancing profits, and also enhance revenue sources (in case there is a recovery of the bad asset). This will help banks to enhance and increase credit lendings.

GROWTH DRIVERS

- As per reports, only 2 out of 21 PSB were profitable in 2018, but in 2021, only 2 banks showed losses. Certain key reasons which have been specified is the recapitalization of PSBs and merger of small PSBs to larger ones. Mergers of public sector banks aided in reducing operation costs for the banks. The government’s decision to consolidate public sector banks, which came into effect on April 1, 2020, created fewer but larger banks with more financial strength, better international competitiveness and an ability to support larger lending volumes.

- The banking sector continues to receive government support through various initiatives to promote financial inclusion in the country. For instance, the Pradhan Mantri Jan Dhan Yojana, launched in 2014 as one of the flagship programmes under the financial inclusion agenda, has seen continuous progress across various metrics such as the number of account openings, the number of operating accounts out of total accounts opened, total and average deposits, and issuance of Rupay debit cards.

- Increased Demand for infrastructural investment- The power industry followed by the road sector are the main users of bank credit. India’s power generation sources range from conventional sources such as coal, lignite, natural gas, oil, and nuclear to viable unconventional sources such as wind, solar, agricultural and household waste and hydropower. The demand for electricity in the country has increased rapidly and is expected to increase further in the coming years.

- Growth in Non-Banking Finance Corporations (NBFC) sector to support demand for credit - Among services, the NBFC sector hinges on bank credit for its functioning. Since NBFCs do not have the traditional routes of sourcing funds for disbursing credit, they raise almost all of the funding requirements from banks for on-lending. As a result, NBFCs remain an important demand driver for banks to lend to.

- Retail loans to continue their growth trajectory

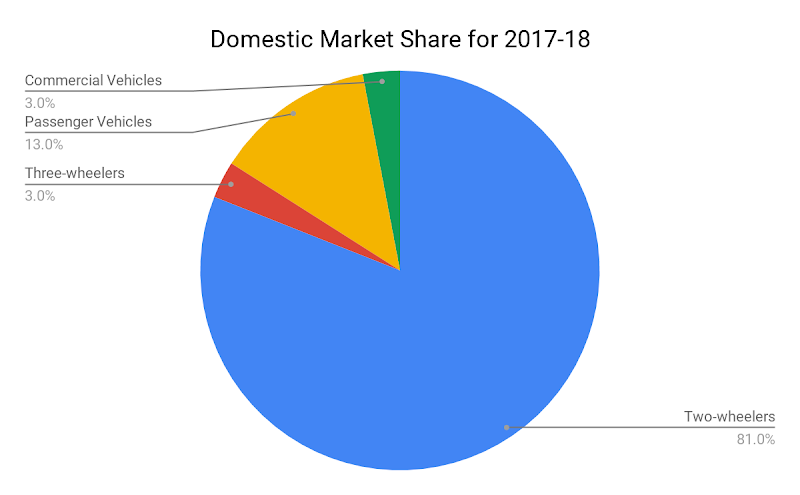

- Vehicle loans - India was 5th largest auto market in 2020. Domestic automobile production has increased from at a CAGR of 2.36% between FY16-20 around 26.36 million vehicles manufactured in the country. The Indian automotive industry is estimated to reach $ 300 billion by 2026. Higher consumption of automobiles will lead to need for bank financing which is expected to help support credit growth.

- Consumer Electronics- The appliances and consumer electronics industry is expected to double to reach Rs. 1.48 lakh crore by 2025. Union Cabinet approved the Production-Linked Incentive (PLI) scheme in 10 key sectors (including electronics and white goods) to boost India’s manufacturing capabilities, exports and promote the ‘Atmanirbhar Bharat’ initiative. Demand growth is likely to accelerate with rising disposable income and easy access to credit.