Renewable energy and transition to clean fuels is a top priority for the global leaders and countries. Pledges made during COP 26 at Glasgow re-affirm the commitments of various countries to reduce carbon emissions globally. The motto is to act locally and think globally. India is the third-largest renewable energy producer in the world. India’s announcement that it aims to reach net zero emissions by 2070 and to meet fifty percent of its electricity requirements from renewable energy sources by 2030 is a hugely significant moment for the sector. India also has a target of achieving 500 GW of renewable energy by 2030 which means that annual capacity addition of 40-50 GW would be required to meet the 500 GW target by 2030.

According to the Central Electricity Authority, by 2030, India's power requirement will touch 817 GW, more than half of which would be clean energy, and 280GW would be from solar energy alone.

Focus on Solar Energy

Solar energy technologies will play a unique and central role in achieving India’s 2030 goal. Installed capacity of solar energy in India has increased from 2.63 GW in March 2014 to 49 GW in December 2021. After a decade of innovation and cost reductions, solar energy sector has evolved to a major source of energy, and it could potentially serve 30% or more of India’s electricity demand by 2030. Solar is already the lowest-cost form of electricity generation in an increasing number of locations in India (Utility-Scale Renewable Tariffs). Drivers for falling solar tariffs include decline in module costs, increasing economies of scale and improvement in technology leading to higher capacity utilization factors (Bifacial solar modules and substrate changes).

Solar energy is highly modular and capable of being deployed cost-effectively at utility scales to power cities and small enough to power individual households (Distributed Solar). Solar energy can play diverse roles, such as directly decarbonizing electricity end uses in buildings, industry, and transportation through the EVs.

Solar is an effective technology for energy production, but effective widespread deployment also requires changes in grid operations and long-term planning. The Indian electric grid is one of the world’s largest networks, comprising millions of miles of transmission and distribution lines that connect thousands of large-scale electricity stations to end users. We have added on an average 50 million people to the grid each year in the last decade. The grid has undergone tremendous change in the past decade, in part due to innovations in the renewable energy sector. One key challenge is that the energy from solar is variable, meaning that output depends on the availability of sunlight. Variable renewable energy cannot, on its own, generate electricity to always meet demand and provide electricity to national grid. This is one of the limitations of solar as well as wind energy, however, in future grid base load planning can be done from other energy sources such Green Hydrogen and Fuel Cells. Various other options are also typically considered for this. For example, some fossil fuel plants would likely remain in use to ensure flexibility of the grid, and their use would need to go together with advanced storage technologies, natural gas-based energy, as well as demand management and long-distance interconnections to pool renewable assets across a larger geographic area. Completely decarbonizing the grid while maintaining reliability will require a diverse portfolio of zero-carbon generation sources such as Green Hydrogen, thermal plants either with carbon capture and storage or burning clean fuels.

Policy support from Government

India’s solar module manufacturing capacity is set to increase by 4 times in 2025 as compared to 2021, with 30-35 GW of fresh module capacity set to be commissioned following strong demand, favourable policies, likely improvement in energy efficiency, and price competitiveness.

Government has also supported domestic manufacturers through various policy measures. The imposition of basic customs duty (BCD) on imported solar cells (25%)/ modules (40%) is to promote domestic manufacturing by making the domestic cells/modules competitive. This will increase the project costs in the short term however to take care of the potential increase in costs and keep the domestic solar industry competitive, government has allocated incentives under the Production Linked Incentive (PLI) scheme for the solar module manufacturing sector. These actions will reinforce the vision of “Atmanirbhar Bharat” in the Solar Module manufacturing sector.

Government has also announced dedicated corridors to evacuate renewable power through Phase-2 of the Green Energy Corridor (20 GW). The Green Energy Corridor Project is one of the initiatives of government to encourage renewable energy integration with the national grid.

Employment Generation

India can potentially create about 3.4 million jobs (short and long term) by installing 238 GW solar and 101 GW new wind capacity to achieve the 500 GW non-fossil electricity generation capacity by 2030. These jobs represent those created in the wind and on-grid solar energy sectors. A workforce of about one million can be employed to take up these green jobs.

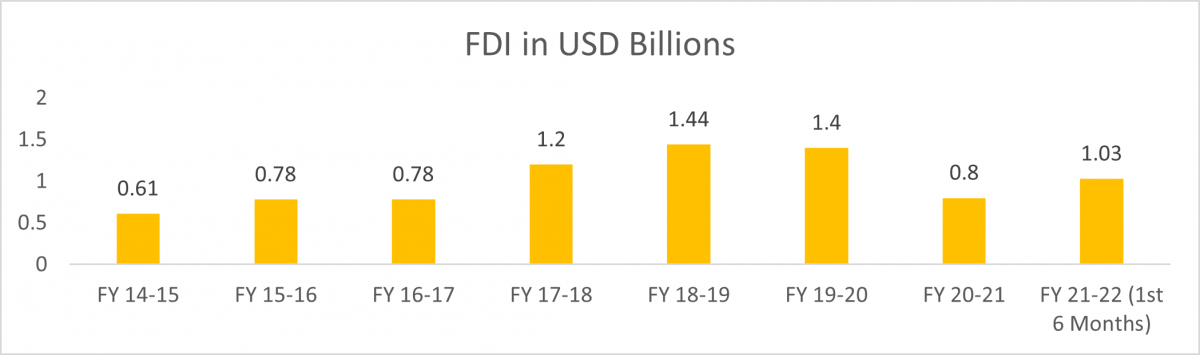

Investments in the Renewable Sector

Majority of the renewable expansion in the country has been possible with the help of attractive FDI opportunities in the sector and established achievable targets which led to gradual increase of FDI in India. The renewable energy targets set by governments have helped the investors to make an informed choice and gives them policy stability assurance for the future. The sector has received a cumulative FDI of $ 8 Billion since 2014 till Sept’21. We are on track to achieve FDI of $ 1.5 Billion in the current fiscal year.

The Way Ahead

The investments required to achieve the goal of 500 GW renewable energy by 2030 requires a concerted approach by the private as well as public stakeholders. On a very conservative capital funding calculation ($ 0.5 Billion/GW for renewable (Solar (280 GW) and Wind (140 GW)), the investments required for achieving the target is approximately $ 210 Billion – an average of $ 23 Billion investment is required each year in the sector to achieve the target. Investments on this scale will help us achieve the targets within the timelines. It can help India meet the climate goals set in the Paris Agreement and position us to seize new opportunities in renewable energy sector.

Achieving these goals is within our reach. A low-carbon pathway would not only initiate the significant emissions reductions needed to halt climate change but also create more jobs and economic growth than a high-carbon pathway would.

A combination of near-term and long-term initiatives can have a significant positive impact on India’s economy and its growth. Well-designed and target oriented policies and funding can bend the curve downward on emissions and push the economic growth curve upward, helping secure a more prosperous, secure, and resilient future for India.

- https://www.ceew.in/publications/indias-expanding-clean-energy-workforce

- https://cea.nic.in/old/reports/others/planning/irp/Optimal_mix_report_2029-30_FINAL.pdf

- https://www.crisil.com/en/home/newsroom/press-releases/2022/01/solar-module-making-capacity-set-to-soar-400-percent.html

- https://www.iea.org/reports/india-energy-outlook-2021